Being a digital nomad offers the freedom to work, travel, and immerse oneself in diverse cultures. Yet, like any lifestyle choice, it presents unique challenges–especially in managing finances.

Financial management can seem daunting, with inconsistent incomes, varied expenses, and intricate tax laws. But, with the right strategies, handling money can become as straightforward and enjoyable as your travel experiences.

Financial Hurdles of Nomad Life

First, let’s list the issues digital nomads face. Next, we’ll talk about managing finances:

1. Earnings Uncertainty: Many nomads rely on freelancing, leading to inconsistent monthly incomes.

2. Cost of Living: The cost of living can vary significantly based on the nomad’s location. For example, the cost of living in a place like Tokyo could be much higher than in a city like Bali.

3. Tax Complexity: Tax situations for digital nomads can be complex based on their home and current country’s laws. Some people might even have to pay taxes in more than one place.

Recognizing these challenges is the first step toward effective financial management.

Setting Up a Solid Financial Foundation

You need a strong financial foundation to make it through the financial hurdles of the digital nomad lifestyle. Here’s how to start:

1. Emergency Fund: This is a crucial safety net. The size of the fund depends on personal comfort, but a general rule of thumb is to have 3-6 months’ worth of living expenses set aside. This can provide a buffer during lean periods or unexpected expenses.

2. Regular Savings: Apart from your emergency savings, put aside some of your income every month. This can help with big goals like buying a home, getting more education, or setting up a business.

3. Diversified Income: Having more than one source of income can help mitigate the impact of job loss or reduced income from one source. This can include passive income sources such as rent from a leased property, stock dividends, or side business income.

Smart Budgeting Tips

Lily started her digital nomad journey with no clue about budgeting. Within a few months, she ran out of money in the middle of her Europe tour. She got help from a kind local, which made her promise never to travel again without a clear budget.

Smart budgeting is one of the most important ways for digital nomads to manage their money. Here’s how to do well:

1. Expense Tracking: Start by understanding where your money goes. This could track all your expenses, from accommodation and meals to coworking spaces and travel costs.

2. Budget Methods: Opt for strategies like zero-based budgeting or the 50/30/20 rule.

3. Using Budgeting Tools: There are a lot of digital tools and apps that can help you make a budget. Apps like Mint or You Need a Budget (YNAB) can automatically track your expenses, categorize them, and help you set and stick to your budget.

Keep in mind, effective budgeting involves regular reviews and adjustments to your income, expenses, and goals.

Tax Complexities for Digital Nomads

Taxes are often different for digital nomads. While some may be eligible for Foreign Earned Income Exclusion (FEIE) in the US, others may find themselves liable for taxes in multiple countries. Not only it is important to know what your tax obligations are for legal reasons, but it can also help you pay less in taxes.

1. Tax Residency: Each country has its own rules for determining who must pay taxes there. Most of the time, they consider you a tax resident of a country if you spend over 183 days there in a year. But some countries have tax deals that keep them from being taxed twice.

2. Tax Benefits: Some countries have tax deals for remote workers. For example, Portugal has an NHR program exempts certain foreign income from taxes.

3. Seeking Professional Help: Navigating tax complexities often needs expert help.

Remember that while paying as little tax as possible is essential, it’s even more important to follow the tax rules of all the countries that matter.

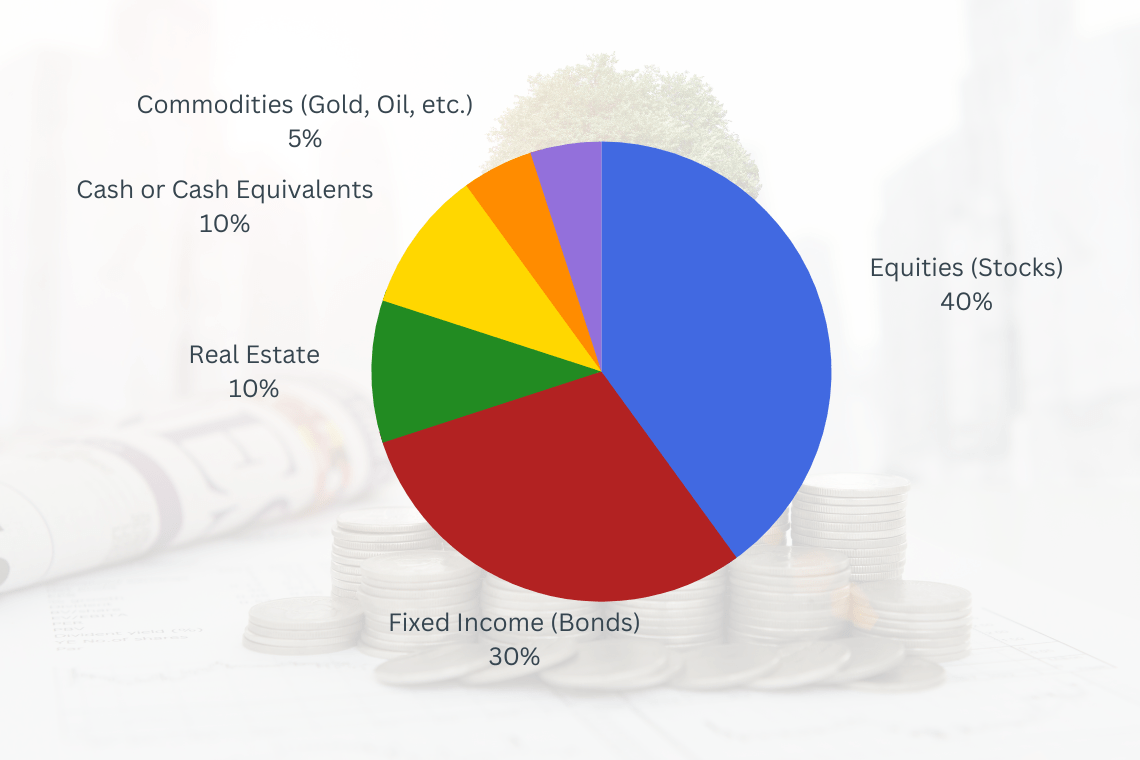

Investments & Retirement: Future-Proof Your Finances

Carlos, an experienced digital nomad, regretted not investing in his early life. Even though he liked the perks of being a nomad, he didn’t have enough money saved up as he got closer to retirement. Now, he mentors younger nomads to start their investment journey as early as possible.

Even if you’re enjoying the digital nomad life, thinking about retirement might feel far away. But it’s good to start early. Here are some tips:

1. Explore Investment Avenues: Invest in stocks, bonds, real estate, and mutual funds. Each has its level of risk and profit. So, it’s essential to do your study. And choose investments that align with your risk tolerance and long-term financial goals.

2. Retirement Savings: You can put money in retirement funds even as a digital nomad. If you’re from the U.S., look into IRAs or Solo 401(k). They can save you on taxes.

3. Flexible Plans: Make sure your retirement plan can change if needed. Think about having different investments or buying things you can easily sell later.

Insurance and Health Care

Elena had a big medical bill in Vietnam. She learned the hard way about having good insurance. As a digital nomad, getting insured is super important.

A nomadic lifestyle demands robust insurance. It’s not just about health; it’s also about protecting your assets and plans.

1. Global Health Insurance: Many digital nomads go for global health insurance. Firms like Cigna Global have plans tailored for expats and long-term travelers.

2. Travel Insurance: Ensure you’re insured for travel mishaps. Popular choices are World Nomads.

3. Property Coverage: Protect your expensive stuff like laptops or cameras from theft or damage.

Halal-compliant Takaful insurance is an option for Muslim digital nomads per Islamic law principles.

Take Advantage of FinTech

Traditional banking can be a challenge for nomads. FinTech makes it easier, offering solutions for transfers, banking, and more. Pick ones that align with your needs and goals, and always check their security standards.

1. Easy Transfers: Use services like Wise, Payoneer, or ACE to send money easily.

2. Neo-banks: Banks like N26 and Revolut are great for nomads. They give good exchange rates and free ATM use.

The key is to choose FinTech solutions that fit your lifestyle and financial goals. Don’t forget to check the security features to ensure your financial data is safe.

Currency Wisdom: Retain Your Money’s Value

Your happiness will fade quickly when you see you are losing money because of poor currency exchange rates. Managing currency isn’t just about numbers; it’s about keeping the worth of the money you’ve earned.

1. Awareness is Key: Keeping a close eye on the currency exchange rates can mean the difference between a standard meal and a gourmet feast.

2. Stay Updated: Apps like XE Currency can help. They update you in real-time and can also forecast potential fluctuations, helping you plan better.

3. Local Currency: Sometimes, you might get a better exchange rate if you take local currency. ATM fees could be a problem, but some cards (which we’ll talk about next) can save the day.

Right Card for Global Spending

Imagine James, who set out for a six-month trip across Asia. In Bangkok, James faced payment difficulties as his primary credit card was declined, and his backup card charged high fees. Don’t be James.

1. No Foreign Fees: Cards that don’t charge foreign transaction fees can save your life. They ensure more of your money stays with you rather than with the bank.

2. Always Have a Backup: Always travel with a secondary card. With a secondary card, you won’t face any issues if the first one gets lost or faces acceptance issues.

If you lose or someone steals your card, take immediate action to prevent misuse. And call the emergency helpline numbers or use the online process to freeze or block the card.

Protect Your Digital Assets

In the age of digital banking, we prefer online transactions things, while ensuring the safety of your financial data is very important. This is even more important for digital nomads, who often switch between Wi-Fi networks and deal with client information.

For example, someone hacked Nathan’s bank account after he connected to it through a public Wi-Fi network at a café in Prague. The whole thing was stressful, and it taught him not to let his guard down, especially when dealing with money on a public network.

Use a Reliable VPN

This tool hides what you do online, making it challenging for hackers to see your info.

Recommendation: Services like NordVPN or SurfShark offer strong encryption and many server locations.

Enable Two-Factor Authentication (2FA)

This is an extra security step. It asks for two proofs of identity.

Tip: Use authentication apps like Authy or Google Authenticator for added security over SMS-based 2FA.

Regularly Monitor Your Accounts

Consistently check your bank and credit card statements for any suspicious activity. Many banks also offer real-time transaction alerts to help you stay informed.

Use Secure Password Managers

Avoid using the same password across multiple platforms. Password managers like LastPass or NordPass can generate and store complex passwords, ensuring each account has a unique, strong password.

Avoid Public Wi-Fi

Public Wi-Fi networks, like those in cafes or airports, are often unsecured and can be hotspots for cyber-attacks. If you must use them, avoid accessing sensitive data or making financial transactions.

Best Practice: Always choose secured networks with passwords, and if possible, use your hotspot.

Stay Updated

Cyber threats grow continuously. Updating your software, apps, and devices ensures you benefit from the latest security patches and updates.

Conclusion

Using the right tools and planning wisely as a digital nomad can make your financial life much easier and less stressful.

The digital nomad lifestyle is not only about working from anywhere but also about living without financial stress.

Start managing your finances now and embrace a truly free digital nomadic life.

{kind=link}